Loan EMI Calculator (Car, Personal, Home, Mobile/Laptop, Education

Taking a loan is easy. Managing it smartly is where most people struggle.

That’s exactly where an EMI calculator becomes useful.

With our Loan EMI Calculator, you can quickly figure out how much you’ll need to pay every month — whether it’s for a car, a personal loan, a home loan, or even a small gadget purchase.

Just enter a few details like your loan amount, interest rate, and tenure, and you’ll instantly get a clear picture of your monthly commitment.

No complicated math. No guesswork. Just clarity.

What is EMI (and Why It Matters More Than You Think)

EMI stands for Equated Monthly Installment. It’s the fixed amount you pay every month until your loan is fully repaid.

But here’s what many people don’t realise:

👉 EMI isn’t just a number — it directly affects your monthly budget, savings, and lifestyle.

Each EMI has two parts:

- A portion that repays your loan (principal)

- A portion that goes as interest to the lender

In the early months, you’re mostly paying interest. Over time, you start paying off more of the actual loan.

Understanding this simple concept can save you thousands — sometimes even lakhs — over the life of a loan.

How EMI Actually Works (Simple Breakdown)

Let’s keep this simple.

Your EMI depends on three things:

- Loan Amount – How much you borrow

- Interest Rate – What the bank charges

- Tenure – How long you take to repay

Now here’s the interesting part:

- Longer tenure → lower EMI but higher total interest

- Shorter tenure → higher EMI but less total interest

So it’s not just about “affordability” — it’s about making a smart financial decision.

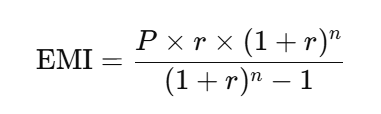

EMI Calculation Formula

Here, P, R, and N are the key variables. This means the EMI amount will vary each time you adjust any of these three. Let’s understand them in detail:

- P refers to the Principal Amount — the original loan amount provided by the bank, on which the interest is calculated.

- R stands for the Rate of Interest determined by the bank.

- N represents the Number of Years allotted for loan repayment. Since EMIs are paid monthly, the tenure is converted into the number of months.

Why You Should Always Use an EMI Calculator Before Taking a Loan

Most people make this mistake: They take a loan first… and think about EMI later. That’s backward approach.

Here’s what a good EMI calculator helps you do:

Plan Before You Commit

- You know your EMI before signing anything.

Avoid Over-Borrowing

- Just because a bank offers ₹10 lakh doesn’t mean you should take it.

Compare Multiple Scenarios

- Try different tenures, rates, and amounts — see what works best.

Stay Financially Stress-Free

- A manageable EMI = peace of mind every month.

EMI Calculator for Different Loan Types

Not all loans are the same — and neither are their EMIs.

Let’s break down the most common ones.

🚗 Car Loan EMI Calculator

Buying a car is exciting. But financing it blindly? Not so much.

Car loan EMIs usually depend on:

- On-road price

- Down payment

- Loan tenure (typically 3–7 years)

Most interest rates fall between 8% and 12%.

💡 Practical tip:

If you can increase your down payment even slightly, your EMI drops significantly.

🏍 Bike Loan EMI Calculator

Bike loans are smaller, but people often make poor decisions here.

Why?

Because “EMI looks small”.

But:

- Interest rates are slightly higher

- Tenure is shorter

👉 A ₹1 lakh loan might look cheap monthly — but over time, you still pay extra interest.

📱 Mobile & Laptop EMI

“Zero-cost EMI” sounds attractive.

But read the fine print.

In many cases:

- Discounts are removed

- GST on interest is added

- Processing fees apply

👉 You may still end up paying more than expected.

🚛 Commercial Vehicle Loan EMI

These loans are typically taken for income generation.

- Trucks

- Lorries

- Transport vehicles

Here, EMI isn’t just an expense — it’s part of your business.

💡 If your vehicle generates steady income, a slightly higher EMI can still make sense.

🎓 Education Loan EMI

Education loans are different.

Most come with a moratorium period:

- You don’t pay EMI while studying

- Repayment starts later

Sounds good — but remember:

👉 Interest keeps adding during this period.

💼 Business Loan EMI

Business loans depend heavily on:

- Cash flow

- Credit profile

- Business stability

There’s no “one-size-fits-all” EMI here.

👉 The key is aligning EMI with your monthly revenue.

💰 Personal Loan EMI

This is where most people go wrong.

Personal loans are:

- Easy to get

- Fast to process

- Expensive

Interest rates can go up to 18–20%

👉 Always calculate EMI before taking one — not after.

Real-Life EMI Examples

Understanding EMI becomes much easier when you look at real-world situations. Below are practical examples across different loan types to help you see how EMI actually works.

🚗 Car Loan EMI Example (Mid-Range Car Purchase)

Let’s say you’re planning to buy a car worth ₹12 lakh.

Loan Details:

- Car Price: ₹12,00,000

- Down Payment: ₹2,00,000

- Loan Amount: ₹10,00,000

- Interest Rate: 9% per annum

- Tenure: 5 years (60 months)

👉 EMI Calculation:

- Monthly EMI ≈ ₹20,758

- Total Payment ≈ ₹12,45,480

- Total Interest Paid ≈ ₹2,45,480

🧠 What This Means:

- You pay around ₹20k every month

- Over time, you pay ₹2.45 lakh extra as interest

👉 If you increase your down payment by ₹1 lakh:

- Total interest reduces significantly

- EMI drops to ≈ ₹18,683

💰 Personal Loan EMI Example (Emergency Expense)

Suppose you take a personal loan for ₹5 lakh.

Loan Details:

- Loan Amount: ₹5,00,000

- Interest Rate: 13%

- Tenure: 3 years (36 months)

👉 EMI Calculation:

- Monthly EMI ≈ ₹16,800

- Total Payment ≈ ₹6,04,800

- Interest Paid ≈ ₹1,04,800

🧠 Insight:

- Personal loans are expensive

- Even small interest differences matter

👉 At 11% instead of 13%:

You save around 15 to 17 thousands with just change in the interest rate

🏍 Bike Loan EMI Example (Budget Purchase)

Planning to buy a bike worth ₹1.2 lakh?

Loan Details:

- Bike Price: ₹1,20,000

- Down Payment: ₹20,000

- Loan Amount: ₹1,00,000

- Interest Rate: 11%

- Tenure: 2 years (24 months)

👉 EMI Calculation:

- Monthly EMI ≈ ₹4,660

- Total Payment ≈ ₹1,11,840

- Interest Paid ≈ ₹11,840

🧠 Insight:

- EMI looks small, but interest % is higher

- Short tenure helps reduce interest

🏠 Home Loan EMI Example (Long-Term Loan)

Buying a house worth ₹60 lakh?

Loan Details:

- Property Price: ₹60,00,000

- Down Payment: ₹10,00,000

- Loan Amount: ₹50,00,000

- Interest Rate: 8%

- Tenure: 20 years (240 months)

👉 EMI Calculation:

- Monthly EMI ≈ ₹41,822

- Total Payment ≈ ₹1,00,37,280

- Total Interest ≈ ₹50,37,280

🧠 Insight (VERY IMPORTANT):

👉 You pay more in interest than the loan itself

This is why: Prepayment is powerful. Even 0.5% rate reduction matters

🚛 Commercial Vehicle Loan Example

Buying a truck for business?

Loan Details:

- Vehicle Cost: ₹25,00,000

- Down Payment: ₹5,00,000

- Loan Amount: ₹20,00,000

- Interest Rate: 10%

- Tenure: 5 years

👉 EMI Calculation:

- Monthly EMI ≈ ₹42,500

- Total Payment ≈ ₹25,50,000

- Interest Paid ≈ ₹5,50,000

🧠 Insight:

👉 If the vehicle generates income > EMI

→ Loan is productive

What You Should Learn from These Examples

Across all loan types, a few key patterns emerge:

Interest Adds Up Over Time

- Longer loans = more interest

Small Changes Matter

- 1% lower interest = big savings

- 1–2 years shorter tenure = huge difference

EMI Should Match Your Income

- Never stretch your budget just to afford a loan

Use EMI Calculator Before Final Decision

- Don’t rely on bank estimates

EMI vs Loan Tenure – What Should You Choose?

This is where smart borrowers win.

- If you want lower monthly burden → choose longer tenure

- If you want lower total cost → choose shorter tenure

👉 Ideally, balance both.

Don’t stretch your loan unnecessarily just to reduce EMI.

Common EMI Mistakes to Avoid

Let’s be honest — most people don’t calculate properly.

Avoid these:

- Taking loan based on eligibility, not affordability

- Ignoring processing fees and hidden charges

- Choosing long tenure without thinking long-term

- Not checking floating vs fixed interest

FAQs

What is EMI in simple terms?

It’s the fixed monthly payment you make to repay a loan.

How is EMI calculated?

EMI is calculated based on three factors — loan amount, interest rate, and loan tenure. Instead of calculating manually, you can use the EMI calculator above for instant and accurate results.

Why does my EMI stay the same every month?

In most loans, EMI remains fixed because it is calculated using a standard formula. However, the portion of principal and interest within the EMI changes over time.

What happens if I miss an EMI payment?

Missing an EMI can result in:

a. Late payment penalties

b. Negative impact on your credit score

c. Additional interest charges

It’s always best to pay EMIs on time.

Is it better to choose a longer or shorter loan tenure?

It depends on your financial situation:

a. Longer tenure → lower EMI but more interest

b. Shorter tenure → higher EMI but less interest

Choose a balance based on affordability.

Is EMI calculation the same for all loans?

Yes, the formula is the same. However, interest rates, tenure, and terms differ across loan types.

What is a good EMI to income ratio?

A safe rule is:

👉 Your total EMIs should not exceed 30–40% of your monthly income

This helps you maintain financial stability.